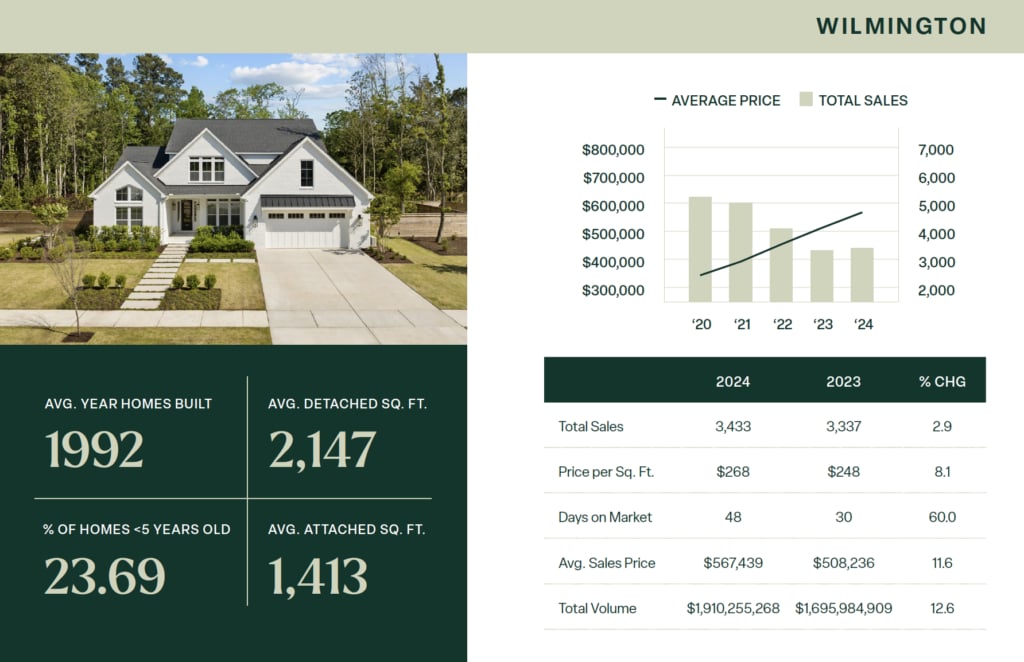

This year, as the market evolved, we seized the opportunity to pause, realign, and refocus our energy, adopting a balanced and intentional approach to navigate the changes with clarity and purpose. The Wilmington area real estate market experienced notable shifts from early January 2024, heading into the election year. Initially, the market faced relatively low inventory levels, a trend that continued throughout the year, keeping competition fierce for available homes. In the first half of 2024, interest rates—having surged in 2023—began to stabilize and even decline slightly, offering some relief to buyers. However, despite the lower rates, the ongoing supply-demand imbalance kept home prices elevated in many segments. The luxury market remained particularly strong, with high-end homes continuing to sell at a premium. As the election year progressed, market uncertainty persisted, though local demand for properties in Wilmington’s desirable neighborhoods remained steady, fueled by ongoing migration trends and the area’s continued appeal.

Our incredible agents produced over $335 million in sales in 2024, more than doubling our luxury sales from 27 to 60 properties—those priced over $900k. With approximately 60 agents, we ranked among the top five real estate companies in the tri-county area. The Wilmington real estate market showed remarkable resilience, continuing to thrive amid economic fluctuations and political uncertainties.

Market Outlook on a National Level

When it comes to housing, expectations shape everything. The fear of missing out—or losing out—often influences our decisions more than we realize. Research shows that financial loss feels twice as painful as financial gain feels rewarding. In 2024, this mindset played a key role in a significant slowdown in home sales. Buyers were told that lower mortgage rates were on the horizon, but those rates never materialized. Sellers held out, hoping new inventory would inspire their next move, but fresh listings remained scarce.

With mortgage rates below 7% for over twenty years, it’s easy to forget that they peaked at over 16.5% in 1981. Since 2022, rates have fluctuated between 6.1% and 7.8%. The ultra-low rates of 3-4% are unlikely to return anytime soon. Despite demand consistently outpacing supply for years, ongoing inventory issues, and relatively stable mortgage rates, buyer confidence has not recovered enough to spark a market rebound. Home sales in 2024 are expected to finish about 5% lower than in 2023, largely due to limited inventory—and increasingly, due to affordability concerns that are shrinking the pool of qualified buyers.

The financial world thrives on predictability, but 2025 promises significant change. With new national leadership comes fresh priorities that will impact markets in unpredictable ways. In this context, we want to highlight some key areas that homeowners and prospective buyers should closely monitor. As housing represents the largest investment for many families, all eyes will be on this sector. For more than seven years, low inventory has dominated housing headlines. Ongoing demand makes it crucial for policymakers to focus on increasing supply. Solutions like deregulation and local zoning changes could help, but they require both time and political will. States like California and Oregon have eliminated single-family zoning requirements in an effort to encourage denser housing. However, the most effective levers for improving construction timelines and costs lie within local jurisdictions.

One wild card for 2025 is the insurance market. In late 2024, Hurricanes Helene and Milton caused an estimated $51 billion-$81 billion in property damage. As storm risks continue to rise across the U.S., private insurers are significantly raising premiums or exiting certain markets altogether. This shift underscores the growing importance of programs like the National Flood Insurance Program, which may eventually need to expand to include fire and windstorm coverage to adequately protect residential investments. Ongoing challenges in obtaining insurance could dampen development and new construction investment in many parts of the country.

Challenges in Homebuilding

Even if regulations ease, construction costs remain a significant hurdle. Publicly traded homebuilder stocks have outperformed the broader market over the past five years, maintaining strong profit margins amid rising home prices. Builders are hesitant to sacrifice these margins, even as affordability pressures continue to grow. Currently, housing costs account for an average of 32.9% of household expenses. Higher interest rates have pushed

homeownership further out of reach for many families, with escalating prices and insurance costs adding to the strain. In response, builders have focused on offering smaller, more affordable homes, but achieving widespread affordability will likely require either lower borrowing costs or real wage growth—neither of which seems imminent.

Affordability Takes Center Stage

The Case-Shiller Home Price Index shows that home values have grown by 94% over the past decade—meaning a $250,000 home in 2014 now costs $485,000. Meanwhile, real household income has increased by only 19.7%, highlighting the widening affordability gap.

Homeowners are pressured to stay in their current homes, partly due to their historically low mortgage rates. More than 70% of current mortgages are below 5%, creating a significant financial incentive to stay put. However, as traditional drivers of resale—such as divorce, job relocations, downsizing, or changes in family size—continue to occur, the lock-in percentage will likely decrease, boosting market activity and creating opportunities for more listings in the future.

The housing market has seen sales drop nearly 30% since 2021, but the potential for recovery remains. To spark growth, inventory must increase—either through new construction or more resale homes. However, true affordability depends on a decrease in borrowing costs. Local governments can help by streamlining the approval process for new builds, but broader economic factors will also play a critical role. If interest rates stabilize or decrease, and if local policies support faster development, 2025 could finally bring the market the boost it needs.